When looking at 2022 from a financial standpoint, the year has been defined by inflation. Cost of goods and services have skyrocketed and despite aggressive raises to the interest rate from central banks, inflation remains concerningly high.

Impact of inflation

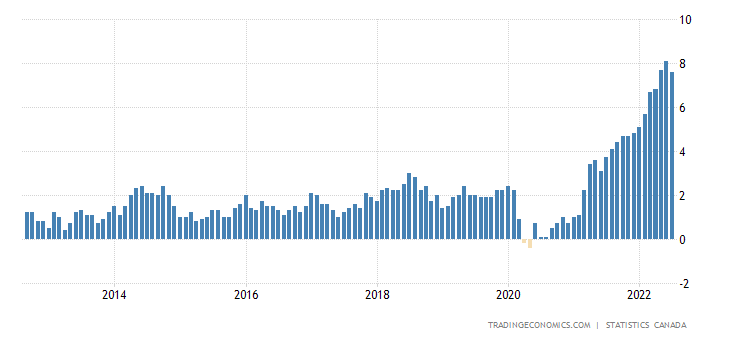

For a visual of how out-of-hand inflation has gotten, here is a chart depicting the inflation rate over the past 10 years:

High inflation erodes consumer purchasing power, leads to higher interest rates and unemployment, and ultimately slows the economy.

High inflation erodes consumer purchasing power, leads to higher interest rates and unemployment, and ultimately slows the economy.

Another alarming realization of an 8% inflation rate is when you apply the Rule of 72. The Rule of 72 calculates how long it will take an amount to double in value based on the current interest rate. With inflation, the Rule of 72 works in reverse: Canadians can calculate how quickly rampant inflation would halve their purchasing power. Example:

72 / (current inflation rate) = # of years until an amount of money loses half its value

72 / 8 = 9 years

Based on an 8% inflation rate, it would take 9 years for purchasing power to be cut in half.

What can Canadians do about high inflation?

Here are some recommendations for Canadians to weather this inflation storm:

- Seek out attractive fixed income options such as GICs, bonds and/or term deposits for savings accounts and emergency funds

Reasoning: A quick google search will highlight some of the best rates on fixed income investments being offered by banks and credit unions for Canadians. While the returns offered are currently below the rate of inflation, the belief is inflation will be dropping at some point soon, so locking in a 5-year bond term (for example) at a 5% annual return looks attractive in the long run. Also, if you have excess funds sitting in a chequing account, now is the time to look at high-interest accounts and other options that offer liquidity and a modest return.

- Maintain investment strategies (avoid reactionary decisions)

Reasoning: Most investors with RRSPs and TFSAs have stock market exposure in one form or another. Now is not the time to get caught up in news headlines about a potential recession or make impulsive decisions because a stock analyst said the S&P 500 will drop “X” percent. As long as your investment portfolio is based on a current investor profile assessment, there is no need to speculate or try to time the market. Stick to your investor profile and follow a dollar-cost average strategy (regularly scheduled, set contributions to your investment account).

- Keep track of budgeting and cash-flow

Reasoning: Reviewing one’s credit card statement or bank account each month can shed plenty of light on spending habits and what, if anything, can be clamped down on. For example, there might be monthly subscriptions you no longer use or a service you didn’t even know you were paying for. Another worthwhile exercise is comparing current expenses versus last year’s. This will provide insights into what expenditures have been the most impacted by inflation, allowing you to become more diligent and tighten up specific budget categories (if applicable).

Want help navigating inflation? We can help. Reach out to Jeff Graham at (604) 363-7549 or jeff@firstoakfinancial.ca.

DISCLAIMER: this commentary is provided for general informational purposes only and does not constitute financial, insurance, investment, tax, legal or accounting advice.