“There are only two certainties in life – death and taxes.” – Benjamin Franklin

Not only does this well-known quote continue to ring true, but the two of them truly go hand in hand. Despite the Canada Revenue Agency not imposing taxes on inheritance (yet) or an estate tax like the United States, taxes on death are still a significant factor for Canadians.

Income inclusion from registered accounts, capital gains, and probate fees are all factors that can deplete the assets people spent their life building.

To demonstrate the affect this can have on an estate (& the beneficiaries), take a look at this Case Study:

Assumptions Made:

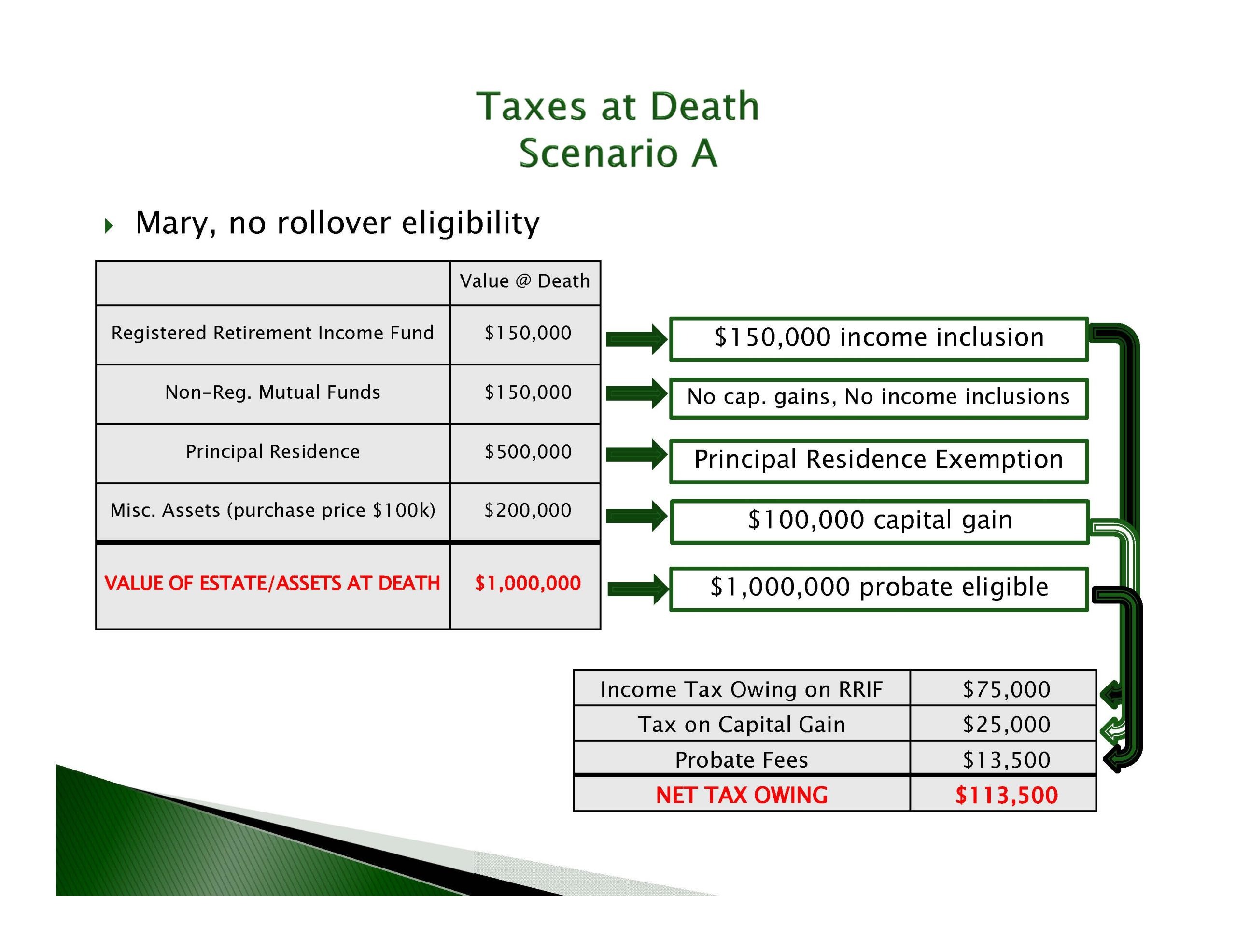

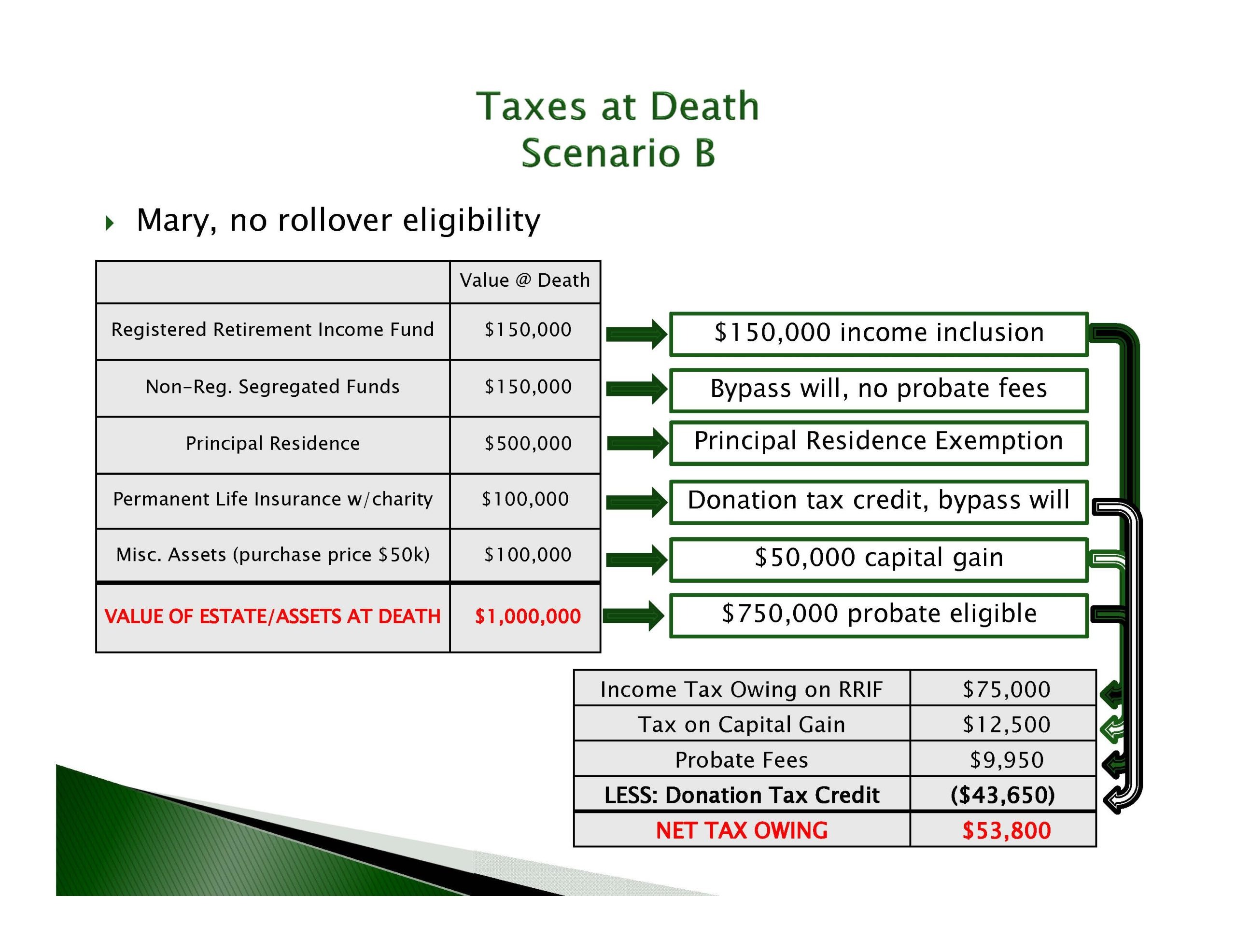

Assumptions Made:1. Mary has no rollover eligibility, meaning no spouse or financially dependent child/grandchild with a mental or physical disability.

2. The mutual funds/segregated funds have not increased in value.

3. Miscellaneous assets could be artwork, coins, jewelry or other personal property that appreciates in value.

1. At the time of executing the estate planning strategies, Mary was insurable.

EXPLANATION:

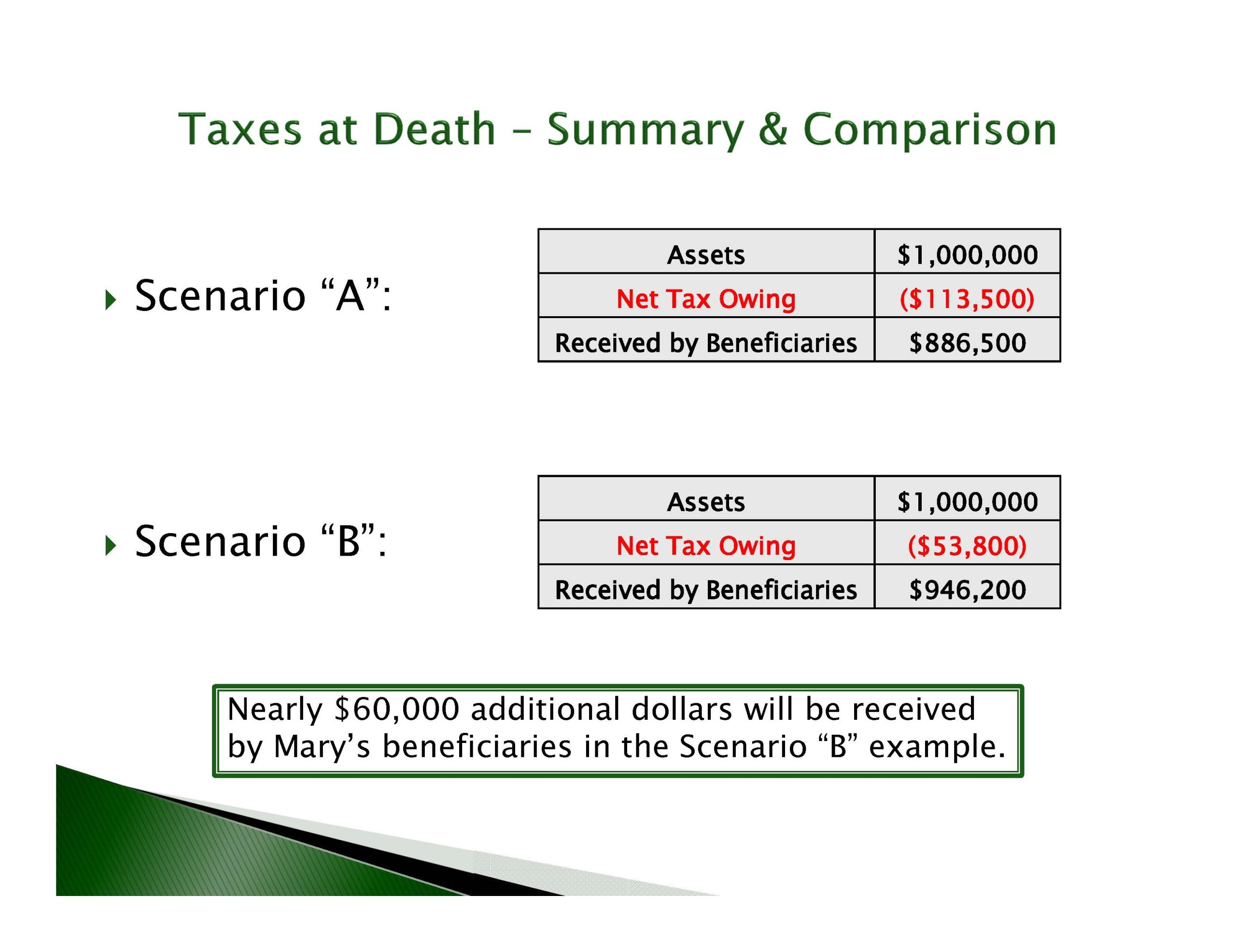

By implementing TWO simple Estate Planning strategies, Mary is able to leave her beneficiaries an extra $60,000, which would have otherwise gone to the Canada Revenue Agency:

- Convert her mutual funds (Scenario A) into segregated funds (Scenario B), bypassing the lengthy, public probate process and the accompanying probate fees.

- Selling half of her miscellaneous assets (Scenario A) and re-allocating the funds into a permanent life insurance policy with her favourite charity named as the beneficiary (Scenario B). This provides a donation tax credit on her death and ultimately leads to immense tax savings. Most importantly, Mary has left a lasting legacy to a cause she feels strongly about.

This is a very simplistic example of the taxes at death that Canadians can expect. Through basic estate planning strategies, substantial tax savings can be realized. Talk to Jeff Graham to learn more – he can be reached at jeff@firstoakfinancial.ca or (604) 363-7549.

DISCLAIMER: this commentary is provided for general informational purposes only and does not constitute financial, insurance, investment, tax, legal or accounting advice.